DeFi lending led a fresh record in crypto borrowing in Q3, with Galaxy Digital reporting that total loans across decentralized and centralized platforms neared $73.6 billion and set a new high above the 2021 peak. DeFis share climbed to 62.7%, highlighting how on-chain tools are outpacing traditional crypto lenders.

Key takeaways at a glance

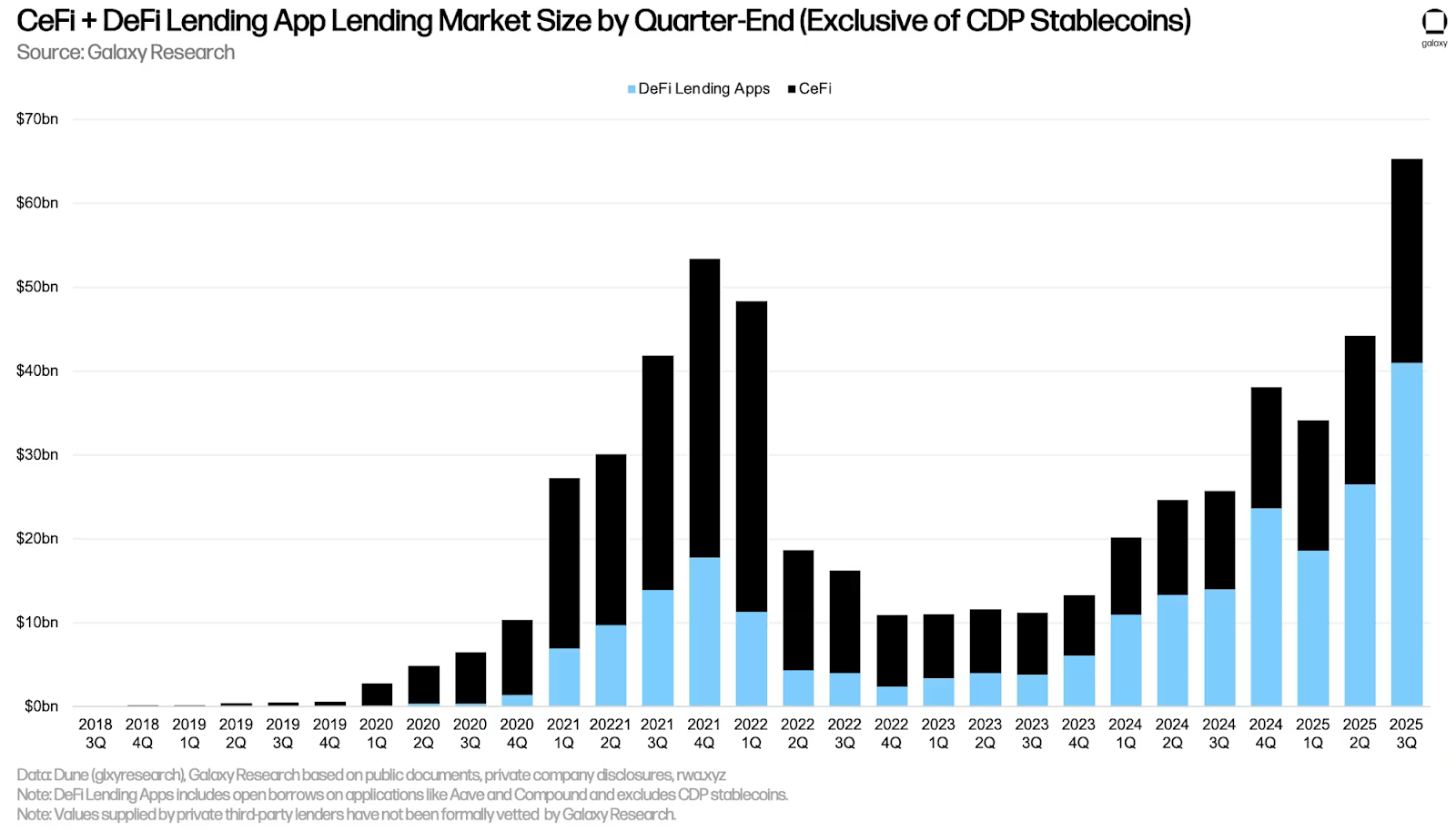

- Total crypto loans: almost $73.6B, a new high above Q4 2021s $69.3B peak

- Quarter-end snapshot: $65.3B in combined DeFi + CeFi loans, up $21.1B from Q2

- DeFis market share: 62.7% in Q3, up from 59.8% in Q2

- DeFi borrowing growth: +$14.5B in Q3, nearly +55%

Whats driving the surge

Galaxys Q3 State of Crypto report points to a simple recipe: more rewards and stronger collateral. Airdrops and points programs encouraged users to borrow and participate. At the same time, rising coin prices boosted the value of collateral, allowing people to borrow more against the same assets. New collateral options and improved lending products also helped.

Put plainly: when your crypto is worth more, lenders will let you borrow more. Q3 had plenty of that.

Mind the measurement gap

Not all borrowing is easy to track. Galaxy flags a risk of double-counting when centralized lenders borrow on-chain and then lend that money off-chain. In practice, the same dollars can appear in two places.

Example: a centralized lender posts idle BTC as collateral to borrow USDC on-chain, then lends that USDC to a client off-chain. That one loan shows up on-chain in DeFi metrics and on the lenders books. Galaxys team calls out this blind spot and notes that CeFi disclosures are inconsistent and often delayed, making true totals hard to verify.

By the numbers: DeFi vs. TVL

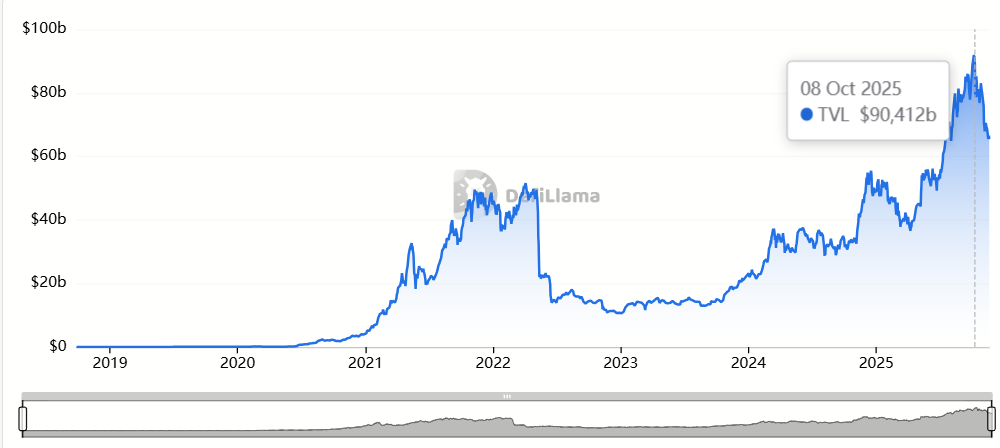

Theres also a gap between borrowing and total value locked (TVL). TVL is the amount of crypto deposited in DeFi apps, not the amount actually borrowed. According to DefiLlama, lending protocol TVL hovered around $90.9B in early Octoberust as Q4 beganuggesting that on-chain activity may have pushed higher right after the quarter closed.

Galaxy clarified that its all-time high language applied to the end of Q3 2025. Early Q4 data indicate activity likely moved even higher after the quarter closed.

Volatility returns after the peak

The new high didnt mean smooth sailing. A sharp market drop on Oct. 10 triggered record daily liquidations across crypto. In early November, the Balancer exploit and the collapse of Stream Finance added fresh stress to DeFi users and liquidity.

Since Oct. 10, total DeFi TVL is down more than 25%, sliding to about $125B from roughly $170B. That retreat underscores how quickly leverage can unwind when prices fall or when trust takes a hit.

Why this matters

- Leverage cuts both ways: Bigger borrowing can lift returns in bull markets and speed up selloffs in downturns.

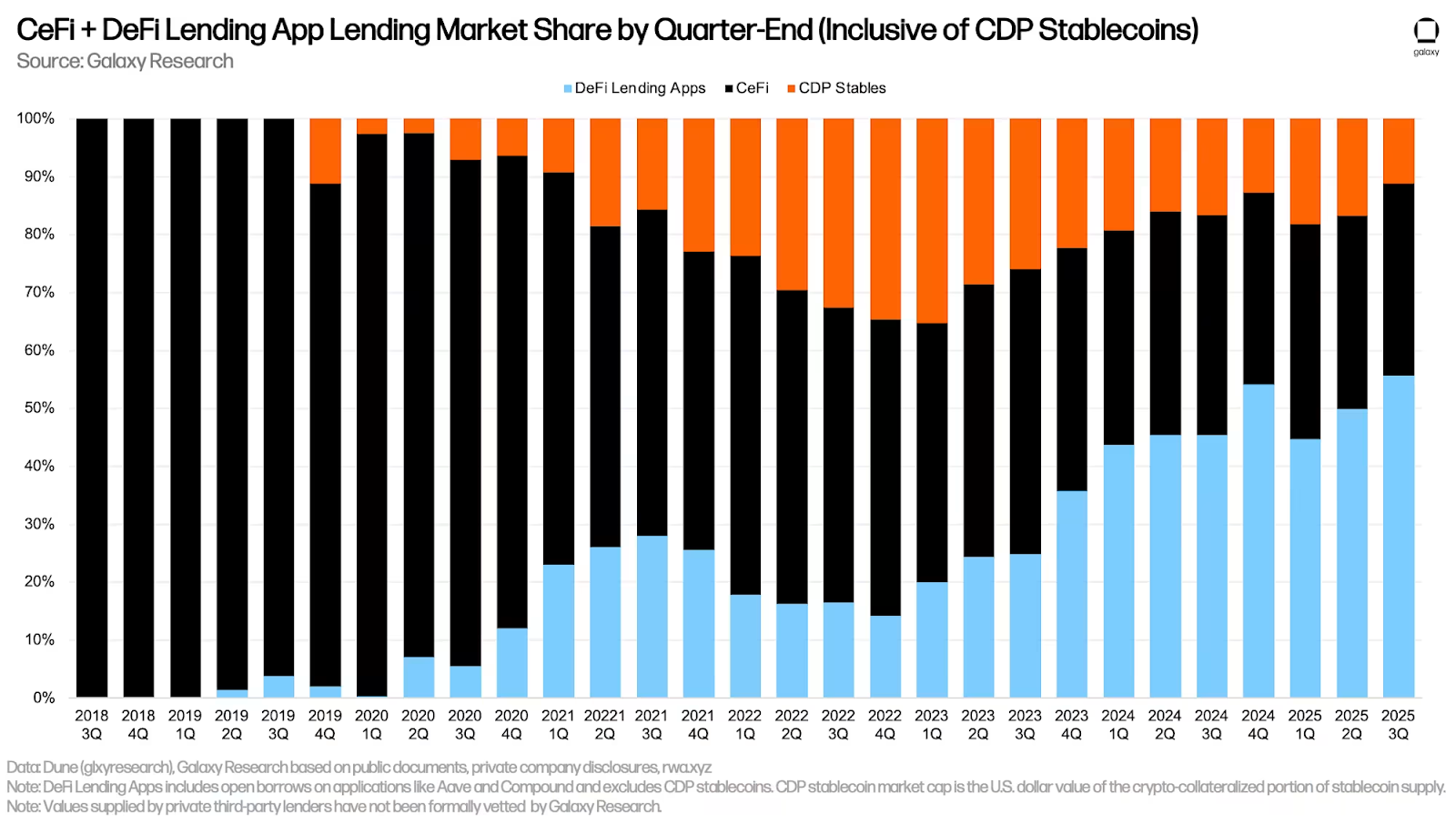

- DeFis rising share: With 62.7% of loans at quarter-end, DeFi continues to chip away at CeFis role in credit markets.

- Data quality risk: CeFi opacity and potential double-counting make it harder for investors to judge real leverage in the system.

What to watch next

- Rewards cool-down: If airdrops and points programs fade, borrowing demand could slow.

- Collateral health: Sustained price gains support borrowing; a drawdown can flip that dynamic fast.

- Transparency push: Clearer CeFi disclosures would reduce the measurement gap between on-chain and off-chain activity.

The bottom line

Q3 marked a high-water line for crypto credit, with DeFi in the lead. But the same forces that fueled the surgeeisurely markets, incentives, rising collateralan also magnify risk when sentiment turns. For everyday users and big investors alike, the takeaway is simple: watch the leverage, and watch the data.