Stablecoins are back in the spotlight after the European Central Bank (ECB) warned they pose a threat to financial stability, especially if a crisis forces the rapid sale of U.S. Treasuries held by major issuers like Tether and Circle.

Key points

- The ECB says stablecoins can lose their peg and trigger runs that spill into traditional markets.

- Tether and Circle hold large reserves in short-term U.S. government debt; forced selling could hit the $25 trillion Treasury market (ECB).

- Interest-paying stablecoins are banned under Europes MiCA rulebook; U.S. banks are pushing for similar limits.

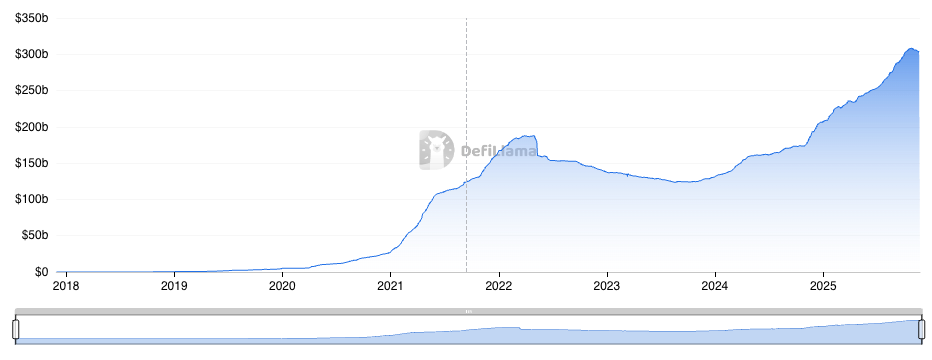

- The stablecoin market topped $300 billion in October, with USDT and USDC making up over 85% of supply (DeFiLlama).

- In the U.S., policymakers are moving toward clearer rules as the Trump administration promotes the country as the "crypto capital of the world."

Why the ECB is sounding the alarm

Stablecoins are crypto tokens designed to track a currency like the U.S. dollar. They hold reserves such as cash and Treasury bills to stay at $1. But if users doubt they can redeem at $1, a "depeg" can happen, and withdrawals can snowball into a run.

The ECB argues that this risk matters beyond crypto. Because major issuers hold large amounts of traditional assets, trouble in stablecoins can quickly move into banks and bond markets.

How a run could hit bonds

The banks core worry: a fast exodus from stablecoins could force issuers to sell their reserves all at once. That "fire sale" can push prices down and pull yields up in the massive U.S. Treasury market, which the ECB pegs at about $25 trillion.

Think of it like many depositors lining up at once: even strong assets can wobble if everyone sells at the same time. With stablecoins plugged into traditional finance, that pressure wouldnt stay inside crypto.

MiCA shuts the door on interest-paying coins

Europes Markets in Crypto-Assets Regulation (MiCA) bans interest-bearing stablecoins. The ECB and many banks say paying yield on tokens could pull deposits out of the banking systema process often called "disintermediation."

U.S. banks have raised similar concerns, pointing to how sudden withdrawals can stress balance sheets, a lesson underscored by past bank runs and the 2008 crisis.

The U.S. leans into rules, not retreat

Despite pushback from some banks, the U.S. continues to engage with the sector. The Trump administration has promoted making the U.S. the "crypto capital of the world." In July, the GENIUS Act passed to tighten oversight of circulating stablecoins, especially those that pay yield, and to address risks tied to Decentralized Finance (DeFi), or financial services built on public blockchains.

By the numbers

The market value of stablecoins topped $300 billion in early October. Two names dominate: USDT (Tether) and USDC (Circle) together account for more than 85% of supply, per DeFiLlama.

What this means

- Bond market ripple risk: If a large stablecoin faces a run, selling its Treasury bills could add stress to a key funding market used by governments, banks, and companies.

- Concentration matters: With USDT and USDC dominating supply, problems at one issuer could have outsized effects across crypto and traditional finance.

- Regulatory split view: Europe is drawing hard lines on interest-paying tokens; the U.S. is building a rules framework while staying industry-friendly.

How to think about the risk

For everyday users, the key questions are simple: Can the issuer redeem at $1 quickly, and what exactly sits in the reserve? For markets, the bigger issue is speedhow fast large positions in Treasuries might need to be sold in a crunch.

The ECBs message is clear: stablecoins are not just a crypto story. Their links to banks and bonds mean any wobble could travel fast, making regulation and transparency more than just box-ticking.