NFT lending is deep in a slump. According to DefiLlama, total value locked (TVL) across NFT loan platforms sits around $8.3 million, down roughly 97% from more than $300 million in March 2024. That puts the sector back near 2022 levels.

By the numbers

- Sector TVL: about $8.3M today vs. 2024 peak above $300M (DefiLlama).

- Blend, the lending product from Blur built with Paradigm: near $3M TVL, down over 90% from more than $115M in early 2024 (Paradigm).

- Arcade, backed by Pantera: around $300K TVL, down more than 98% from a March 2024 high of $21.5M; Arcade raised $15M in a 2021 Series A (PRWeb).

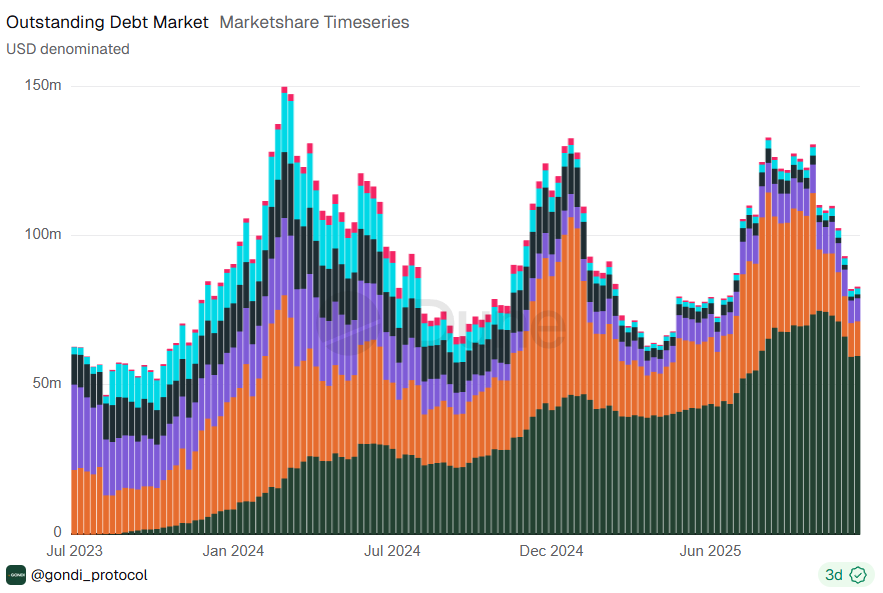

- Outstanding NFT loan debt: down about 45%, from roughly $150M in March 2024 to about $83M now, per a Gondi dashboard on Dune (Dune).

What changed: rewards dried up

The March 2024 peak lined up with heavy rewards on Blurs lending arm, Blend. As those incentives faded, volumes and borrowing activity fell sharply. That pullback dragged the whole category lower.

Nicolas Lallement, co-founder of NFT analytics site NFT Price Floor, said in comments reported by The Defiant that Blends incentive program dominated the market at the time. When rewards slowed, usage slumped and the sector reset.

From avatar loans to art loans

The market mix is shifting. Activity has moved toward Gondi, a non-custodial, peer-to-peer NFT lending protocol. Instead of mostly profile-picture collections and big IP names such as Pudgy Penguins, more loans are being backed by NFT art. Art collections tend to trade like traditional collectibles, which can encourage steadier borrowing and lending behavior.

TVL can mislead. Debt tells a different story

TVL measures how much capital sits in smart contracts. In NFT lending, TVL can shrink fast when liquidity providers exit. Outstanding debt tracks how much borrowers still owe. That metric shows a smaller drop, suggesting people are still taking loans even as available capital thins.

Data compiled by Gondi on Dune shows outstanding debt sliding about 45% from roughly $150M in March to about $83M today. That gap with TVL hints at lenders pulling capital faster than borrowers unwind positions.

Why this matters

- Liquidity risk: Thinner TVL can mean higher interest rates, tighter loan-to-value ratios, and faster liquidations when prices swing.

- Healthier collateral: A shift from hype-driven avatars to art-backed loans could mean fewer sudden defaults and better price discovery.

- Protocol shakeout: Platforms dependent on points and rewards face a tougher road. Sustainable fee models and accurate pricing tools may win out.

- Investor signal: The divergence between TVL and debt suggests users still want liquidity from NFTs, but lenders are more cautious.

What to watch next

- New incentive programs: If major marketplaces reintroduce rewards, usage could spike againor fade quickly once incentives end.

- Pricing and risk tools: Better NFT pricing oracles and appraisals could support higher, safer loan volumes.

- Broader NFT market: A rebound in blue-chip collections could bring lenders back; continued weakness would keep TVL depressed.

- Protocol design: Peer-to-peer models like Gondi vs. pooled lending may show different resilience in low-liquidity conditions.

The bottom line: NFT lendings TVL has crashed, but borrowing hasnt vanished. The sector is smaller, pickier, and shifting toward collateral that behaves more like classic collectibles. If liquidity returns, platforms built for steady demandnot just rewardswill likely be the ones still standing.